NEW FOR 2026: Under the SECURE ACT 2.0, if you have an employee who is 50 years or older and their 2025 FICA-taxable earnings are $150,000 or more, any catch-up contributions to their 401(k) will have to be made to a Roth 401(k) with after-tax dollars.

To enter in this information in Visual ContrAcct please do the following:

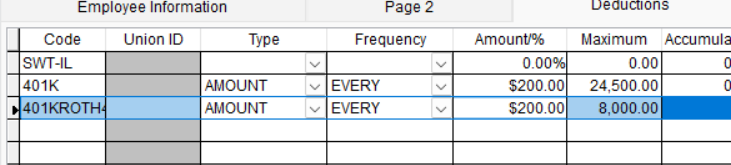

- 1. Create a Roth 401(k) deduction if one does not already exist.

- 2. Add the Roth 401(k) deduction to each employee that made $150,000 or more for tax year 2025.

- 3. The Roth 401(k) deduction maximum column needs to have the difference between the catch up limit and the 401(k) limit of $24,500. This number depends on the age of the employee.

- a. For 50 and older, the limit is $32,500. The number entered into the maximum column needs to be $8,000.

b. For 60 and older, the limit is $35,750. The number entered into the maximum column needs to be $11,250.

b. For 60 and older, the limit is $35,750. The number entered into the maximum column needs to be $11,250.

- 4. On the regular 401(k) deduction maximum column, enter the limit of $24,500